Quantitative easing is leading to investors taking on excessive risk in many asset classes. A great example of the impact of quantitative easing is the Lazarus like rise of Greece from bankruptcy to issuing five year bonds at 4.95% in the space of two years. Normally a country would be locked out of debt markets for at least five to ten years after a default, with some countries taking decades to repair their relationships with overseas lenders and to earn the right to borrow again. Instead investors beat down the door to lend to Greece with €3 billion of bonds issued into apparent demand of €20 billion.

This article uses the 5 C’s of credit to analyse the creditworthiness of Greece. By looking at character, cashflow, capital, collateral and covenants an assessment can be made of the overall risk. The article also combines both behavioural and financial analysis to reach a conclusion about how investors should view the recently issued bonds.

Character: assessing willingness to pay

As a general rule, if the character of the borrower is questionable the lending discussion stops there. Michael Lewis in his book Boomerang described the character of Greece pre-crisis as follows1:

“..what the Greeks wanted to do, once the lights went out and they were left alone in the dark with a pile of borrowed money, was turn their government into a piñata stuffed with fantastic sums and give as many citizens as possible a whack at it.”

In the first bailout in 2010, Greece agreed to sell €50 billion of assets by 2015 to repay some of the outstanding debt. That has since been revised down to €11 billion by 2016 with only €2.6 billion in proceeds received thus far2. Greece has also dragged its feet on implementing structural change, with several “do or die” votes held in the Greek parliament in the last four years on the implementation of further austerity measures. One of these passed by a mere four votes out of three hundred3.

This is not the behaviour of a remorseful borrower; rather it indicates no real change in attitude. Greece has sold a few small assets to appear as if it is doing something, but at the same time it is receiving far more in return from the European Union and the IMF in budget support. There are various estimates of this, but Reuters estimated it to be €42.1 billion in 2012, not long after the second Greek bailout4. I’m not seeing a change in character here at all, rather I think this indicative of pattern that has historically played out with other sovereign debt crises. It is also worth noting that Greece is a serial debt defaulter, with Reinhart and Rogoff noting five events of default or restructure since independence in 1832 spanning more than 50% of the time period since then5.

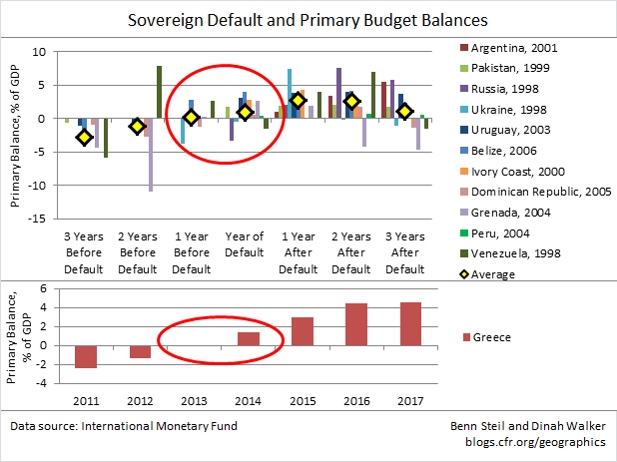

The acid test for Greece is now within sight. The key trigger for many sovereign debt defaults is not when the country starts to have trouble refinancing its debt, but when they reach primary surplus. Primary surplus is achieved when a government raises more in taxes than it spends, other than on interest payments. Greece achieved this in 2013 but it is still well short of a general budget surplus, which includes interest payments.

The combination of political survival and a potentially rebellious population leads many governments to question why they should keep servicing enormous debt loads in a time of high unemployment and economic decline. If there’s a carrot, like IMF or European Central Bank (ECB) funding for pensions, government staff, police and hospitals then a country is likely to play along. However, once the country achieves primary surplus and aid is withdrawn, the attitude can shift to asking why taxpayers should make any meaningful effort to clear the mountain of debt in front of them. Many argue that it was previous governments and overseas investors that allowed this to happen. Thirty years of debt repayments of close to 10% of GDP when unemployment is above 20% just doesn’t seem attractive or fair. The graphic below from Steil and Walker6 graphs this phenomenon for a series of sovereign defaults.

Character assessment then comes down to judgement call on whether the Greek politicians and taxpayers will be willing to prioritise making repayments on their debt over internal spending for decades to come. The regular stream of protests by special interest groups against austerity measures, and the increasing popularity of parties favouring default or further haircuts on existing debts doesn’t augur well. The insistence of outsiders, particularly Germany, that austerity measures must increase and that there will not be any loss of the IMF and ECB loans7 seems like an inevitable conflict. The only carrot I see left is remaining part of the European Union, however the common currency brings its own problems as Greece is unable to benefit from a depreciating currency like other sovereign defaulters.

Cashflow: assessing ability to repay

As noted in the character section, the budget position in Greece is improving but is still a substantial deficit when interest payments are included. The budget deficit in 2013 was estimated to be 4.1% of GDP compared to 9.0% in 2012. With debt to GDP at 174% and an interest rate of 4.95% Greece would need to set aside 8.6% of GDP each year just to meet the interest payments. To amortise the debt over a 30 year period, consistent budget surpluses of 2.5% of GDP are required. Not surprisingly, there is talk of a third bailout being required in 2014, following on from the 2010 and 2012 versions. Media speculation is for €10-20 billion of additional support, with more debt expected to be added to the existing mountain of approximately €410 billion.

Clearly Greece still does not have an ability to pay even the interest on its debts on a standalone basis, with the principal owing increasing further each year. Therefore, the fall-back position is that others will continue to cover the shortfall. That’s starting to sound like a Ponzi scheme, in this case where the IMF, ECB and other bond buyers are assumed to fund the shortfalls for at least the next few years.

Capital: assessing the equity contribution of the borrower

In residential lending, it’s not the end of the road if you are a discharged bankrupt or have missed a few utility bills. Non-conforming lenders specialise in dealing with people who have had credit problems previously. However, the balancing item is that the borrower will need to have more equity to contribute (typically another 10-20% of the property value) compared to someone with a pristine credit history. This aims to ensure that that the borrower is even more incentivised not to default again, whilst reducing the probability of loss and size of any potential loss to the lender. More capital upfront can offset the concern over the borrower’s willingness to repay.

For Greece, the best measure of its relative equity contribution is to compare its government debt to GDP ratio to other countries. On this measure Greece ranks second worst in the world at 174%, beaten only by Japan. Not only is the ratio extremely high, but it has increased from 156.9% in 2012, after the restructure and debt buyback that year reduced the ratio by 50%8.

To most independent outsiders this level is unsustainably high. The much debated 90% threshold put forward by Reinhart and Rogoff for high income countries points towards Greece being seriously impacted for decades to come by having such a high level of debt. If Greece was compared to middle income countries, which is not such a stretch as GDP per capita fell by 31.7% in the 2008-2013 period, then it is again a standout in an ugly way. From 1970 to 2008 there were 36 middle income sovereign defaults with the average debt level pre-default being 69.3%. The current debt to GDP ratio of Greece sits above 34 of the 36 defaults during that time span9. Why would anyone be willing to bet that “this time is different?” If the numbers are not convincing to you here’s a recent quote from a Giorgos Stathakis, a Greek economist who also happens to be a member of its parliament10.

“They are missing the point: Greece does not need a third bailout, it needs debt restructuring.”

Collateral: minimising the loss if the borrower defaults

In the event a default occurs, hard assets such as property or operating infrastructure are preferred. The assets of cashflow businesses (other than the outstanding invoices) are generally not considered as a strong form of collateral. Sovereigns typically don’t pledge any hard assets to support loan repayments, even though they may own a great deal of property and infrastructure assets. As a sovereign, they control the ability of a lender attempting to enforce on any assets within their borders and are strongly incentivised not to give anything away.

When it comes to historical recovery levels, sovereign debt averages recovery levels below loans but in line with other types of bonds. Moody’s study from 2008 found that sovereign debt recoveries had averaged 38% based on the restructured cashflows and 31% based on trading prices shortly after the restructure for the 1983-2007 period. There’s a wide range of outcomes within their data points, from Russia and the Ivory Coast at 18% to the Dominican Republic at 95%11.

In the 2012 debt restructure, 97% of Greece’s bondholders agreed to a 53% loss on face value with the estimated loss based on future cashflows ranging from 55-75%. As senior ranking creditors following the 2010 restructure the IMF and ECB did not suffer principal losses in 2012 but agreed to reduce the interest rates on their loans. Germany in particular has been clear that it will not consider any form of principal loss though it has indicated that other changes such as a reduced interest rate or extended period to repay the loans will be considered.

This raises an additional risk that creditors in most other sovereign defaults have not faced. Incoming bondholders should consider themselves subordinated to the IMF and ECB debt issues, particularly as they have voluntarily lent to Greece with its known and very high risk profile. Together the IMF and ECB obligations amount to approximately 80% of the debt outstanding, or 138% of current GDP. Historical precedents suggest a substantial loss for these lenders should a default occur, with little or nothing available for subordinated bondholders.

Covenants: restrictions to stop the risk level increasing

I haven’t been able to access the bond documents for the recent issue so I will make more general comments in this section. The lack of covenants in bonds relative to loans, and the fact that many bonds are subordinated to loans to the same borrower are the main reasons why recovery rates from loans average roughly double the level of bonds. Corporate loans typically contain solid covenants, although the “cov-lite” phenomenon sweeping the US and to a much smaller extent Europe is changing this for the worse. Well set covenants serve as a handbrake to stop risk levels increasing, by limiting the amount of new debt that can be taken on and creating renegotiation events if the earnings decline materially. By having these restrictions, lenders are able to intervene early, thus reducing both the probability of default and the severity of loss if a default occurs.

Bonds in general and sovereign bonds particularly rarely have good covenant packages. If the borrower makes their interest and principal payments on time, there’s little the lenders can do to stop the borrower from taking on more debt or to force the borrower to balance its budget. The options for lenders who don’t like seeing their risk levels increasing are typically limited to selling the debt, which may come at a substantial loss to the price it was purchased at. Despite all the risk factors identified thus far, there is unlikely to be any meaningful covenants stopping Greece from taking on additional debt or requiring it to implement additional austerity measures.

Conclusion

When assessing Greece against each of the 5 C’s, it not only fails each of them, it fails each of them badly. One negative factor alone may indicate high risk, but five negative factors points to virtually no credit standards being applied. Bond investors are speculating on a highly indebted borrower with a record of recalcitrance and broken commitments, that is currently unable to pay interest let alone principal, likely subordination to other lenders and with few or no covenant protections. It would not be unfair to conclude that the risk characteristics and attitude by the bond buyers to these risks are similar to that of the US subprime sector in 2006.

I believe investors should assess Greece as at least a 50% probability of defaulting in the next 5 years with a close to zero recovery on the bonds in the event of default. If it wasn’t for quantitative easing and the public assertions from Mario Draghi to do “whatever it takes” to keep the European Union functioning I doubt there’d be anyone willing to take the risk at anywhere near the 4.95% yield. No doubt there are some investors who have bought into this transaction with a view to riding the yield a little lower before booking a profit and moving on. I struggle to see this investment strategy as anything other than a classic “pennies in front of the steamroller” trade.

Written by Jonathan Rochford for Narrow Road Capital on April 16, 2014. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Appendices

References

- P44 of Boomerang, Michael Lewis 2011

- http://www.businessweek.com/articles/2014-02-13/greece-may-finally-sell-some-olympic-venues

- http://edition.cnn.com/2012/11/07/world/europe/greece-austerity/

- http://uk.reuters.com/article/2012/11/13/uk-greece-factbox-bailout-idUKBRE8AC0KE20121113

- P99 of This Time is Different, Reinhart & Rogoff 2009

- http://blogs.cfr.org/geographics/2013/12/04/greeksurpluses/

- http://www.ekathimerini.com/4dcgi/_w_articles_wsite3_1_06/04/2014_538756

- http://www.iie.com/publications/wp/wp13-8.pdf

- P23 of This Time is Different, Reinhart & Rogoff 2009

- http://rt.com/business/germany-greece-third-bailout-563/

- https://www.moodys.com/sites/products/DefaultResearch/2007100000482445.pdf