The media sometimes uses the terms “smart money” and “dumb money” to describe institutional and retail investors respectively. The premise is that institutions have full time employees that specialise in various sectors who are well placed to identify mispricing. Retail investors don’t have those resources and are therefore reliant upon shallower (if any) research in making investment calls.

I’ve often used the comparison between non-conforming residential mortgage backed securities (RMBS) and bank hybrids as an example of poor relative value. With the average margin on listed major bank hybrids ending the week at bank bills + 2.25%, the average is now sitting between the spreads on junior AAA and AA RMBS despite preference shares having an equivalent rating of somewhere in the BB or B rating area. (Click here for a primer on credit ratings.) The last RMBS deal issued with these two tranches was RedZed 2019-1, with the pricing at +1.95% (junior AAA) and +2.35% (AA).

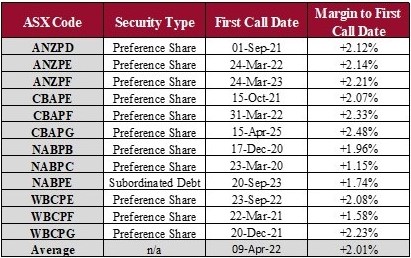

I’ll take the comparison a step further and use the three securities from each major bank that have the smallest spread. (Each major bank has five securities outstanding, making twenty in total.) The average spread of these twelve securities is +2.01% and the average time to the first call date is 2.6 years. For the RedZed deal the weighted average life was 2.1 years for the junior AAA and 3.7 years for the AA.

The summary of this exercise is that the dumb money (retail) is buying and holding sub-investment grade securities that are arguably more equity than debt, whilst the smart money is buying AAA rated debt securities. Despite the massive difference in risk (arguably 26-95 times greater for BB/B preference shares versus AAA/AA RMBS) both groups are getting basically the same return.