The feedback I often get from readers of my articles is that I must be an investment bear. That’s understandable given my last two articles were “The Dirty Dozen Sectors of Global Debt” and “The Coming High Yield Downturn will be Big, Long and Ugly”. However, the performance of Narrow Road Capital recently, and since inception, is one of substantial outperformance of relevant indices, without taking significant risk. I’m also confident in the ability to continue to outperform, even in an environment where many asset classes are overvalued and a widespread correction is possible. How is it possible that a “bear” can position their portfolios for the likelihood of a credit downturn and continue to outperform?

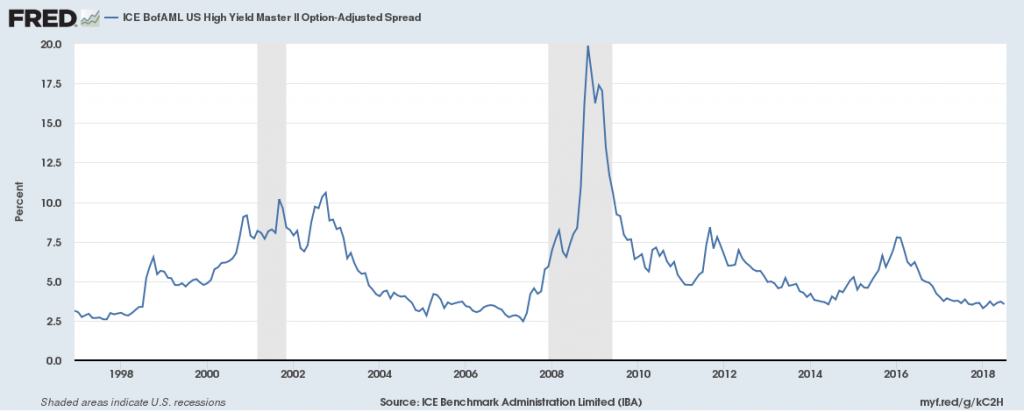

The first part of the answer is that I’m not really a bear, but a realist. The view that markets have had a great run and could either flatline for a while or fall back is pretty common today. In The Dirty Dozen Sectors of Global Debt I outlined that there are many sectors where weaker governments, corporates and consumers are able to borrow with minimal conditions. The graph below of US high yield spreads from the St Louis FRED database is just one example of credit spreads currently being near the bottom of long term ranges.

Examples outside of credit include elevated P/E ratios for US equities, low yields on property and infrastructure assets and aggressive valuations on venture capital backed businesses. It’s certainly possible that asset prices push higher from here but given the starting position the probability of a correction (falls of at least 10%) or bear market (falls of at least 20%) in the medium term is much higher than normal.

Another part that perpetuates the “bear” fallacy is that I frequently write about bad lending. This is partly because credit investing is primarily about figuring out how to lose money and then not doing that. I write articles with the aim of giving readers both something to learn and something to take action on. Writing about sectors in the credit markets where dumb lending is happening is a great way to fulfil both of those aims. By showing readers what credit sectors to avoid, sectors where investors are being paid poorly for the risk they are taking, there’s room to focus on the sectors where outperformance is most likely.

Historical Outperformance

Narrow Road Capital started in mid-2012 and took on its first client in October 2012. The chart below compares performance on all clients in the crossover credit (BBB/BB rated securities) strategy since inception. This strategy has vastly outperformed the Australian investment grade bond index and the US high yield bond index, as well beating Australian equities by a handful of basis points.

The ability to deliver this outperformance without taking outsized risk has been aided by securities that were hangovers from the last downturn. In 2009 and 2010 there were waves of securities traded at enormous discounts to par, that delivered returns in excess of 20% per annum to savvy buyers. By 2012 these “hangover” trades were rare, but two small securities were purchased for clients in 2013 with the largest delivering a net IRR of 33.74%. A 2014 private debt transaction delivered a net IRR of 14.34%, also helping to lift the overall result. Along the way, the bulk of the portfolios have been invested in securities returning 6-8% per annum.

Since early 2017 Narrow Road has also been managing an investment grade portfolio. This has run at around 60% AAA to A rated securities and 40% BBB rated securities. The outperformance has also been substantial.

Achieving these returns obviously requires a focus on securities outside of traditional investment grade government and corporate debt. However, this isn’t a case of increased credit risk driving the results, rather a harvesting of the illiquidity premium available in Australian credit. Some of the securities owned are relatively liquid, others trade infrequently and others are outright hold to maturity securities. Yet with an average credit duration of less than two years on both crossover credit and investment grade strategies, the natural turnover of principal is quite high.

Current Positioning

The portfolios are striking a balance between putting capital to work and earning a strong return whilst ensuring that the capital is available to be redeployed into potentially cheaper assets in the medium term. Rather than chasing returns by lengthening credit and interest rate duration or pushing into lower rated securities, additional return is driven by targeting non-traditional securities with substantial illiquidity premium. This is a natural outworking of the realist view that asset prices are currently elevated but the beginning of a widespread correction could be years away. This balance provides confidence that outperformance can continue to be delivered.

For investment grade, net returns of 4.50-5.00% in the medium term are anticipated. For crossover credit, net returns of 6.50-7.00% are anticipated. These forecasts are based on current opportunities, assuming no mark to market gains or losses and no change in the RBA Cash Rate. That’s a surprisingly positive outlook from a supposed bear.