High Yield Pullback

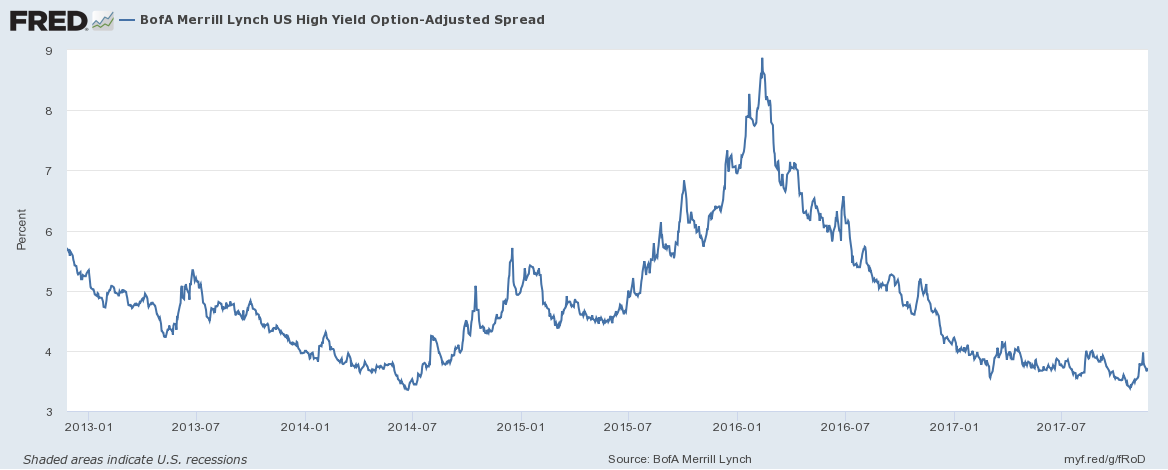

The pullback in high yield credit had more than a few people excited, but it was a very tame affair. As the graph below shows, it was nothing compared to the pullback in early 2016 which was led by energy companies suffering as oil prices fell under US$30 a barrel. This time around the pullback has been focused on a small group of credits with particularly weak fundamentals. Tesla is the most high profile example, a company that burns cash fast but produces cars slowly and whose future products are based on major technological advancements yet to occur. It’s as if investors have woken and realised that negative cashflow companies aren’t good borrowers. This sentiment hasn’t just applied to US high yield credit, sovereigns like Puerto Rico and Venezuela have been hit as well.

Puerto Rico

This month the realisation of how bad things are for Puerto Rico finally hit home. The territory has asked for $94 billion in post-hurricane aid, which if approved could come in the forms of loans rather than grants. This new debt would likely rank senior to the existing debt making existing debt close to worthless. The local government has also flagged that it may need a five year moratorium on principal and interest payments. US legislators are working on a bill that would see the existing debt completely written off. Without extraordinary generosity from the US federal government the bulk of Puerto Rico’s existing debtholders are staring down the barrel of a 0-20% recovery.

Venezuela

The only surprise about Venezuela’s default this month was that the country chose to make payments for so long when the situation was clearly hopeless. Conspiracy theories are being tossed around, the funniest one being that the government is pushing down the bond prices in order to buy them back. That scenario only works if the government has sufficient reserves to repurchase debt, which it clearly doesn’t. Venezuela is so broke it is demanding oil from its joint venture partners for domestic consumption, reducing its only meaningful source of foreign revenue. The first creditors meeting was a shambles, with the few attendees given bags of goodies after sitting through hours of lecturing about the evils of Donald Trump from an alleged drug dealer. Several hedge funds have sold out of their holdings pushing the bond prices down further.

China

After previous warnings turned out to be head fakes, the post-plenum period might hold some real reform for China’s debt markets. Interest rates have been allowed to tick higher, pushing up funding costs for all. Conglomerate HNA has sold one year debt at 8.875%, the highest ever rate for short term US dollar bonds. Investors continue to ignore government warnings that wealth management products can suffer losses, a belief that could soon be tested. Amongst many sectors, poor credit investing is showing up in rail debt, micro lending in rural areas, perpetual debt and even US CLOs where leverage is being applied to juice up returns.