Numerous articles have appeared in the Australian and international media over the last few months suggesting that a bubble in Australian house prices already exists or is at high risk of developing. Low interest rates, sharply rising property prices, and the increasing participation of self-managed super funds using leverage are routinely mentioned as markers of an unsustainable situation. Australian retail investors undoubtedly love to buy residential property and many are comfortable using substantial gearing to make their purchases. Is it possible that twenty years of outsized gains has led them to love residential property too much?

In talking to various market participants this has repeatedly brought up the question of whether Australian Residential Mortgage Backed Securities (RMBS) are at risk. To answer this question I will first review Minsky’s key theory on asset price bubbles and credit cycles and also look at what caused the US house price bubble. Reviewing theory and history together is usually a good start when trying to predict the future, at least in financial markets.

The Theory of Bubbles

To help define when a bubble might exist I always find it helpful to revisit the leading economic thinker on bubbles and credit cycles, Hyman Minsky. Minsky divided leveraged investors into three groups: Hedge, Speculative and Ponzi.

- Hedge investors earn more than enough cash return on their investments to pay interest and thus have cash available to amortise principal on their loans and/or to pay dividends.

- Speculative investors earn only enough on their investment to pay the interest on their loans, so there is effectively no cash available to amortise their loans or to pay dividends.

- Ponzi investors do not earn a sufficient cash return to pay the interest on their loans and thus need to resort to capitalising interest and/or raising more equity to sustain their current borrowings.

Speculative and Ponzi borrowers are effectively betting that their profits will come from rapid asset price growth. Hedge borrowers are cashflow positive from their investments; asset price growth is a welcome but not critical part of their total return.

Due to the cyclical nature of credit provision, Speculative and Ponzi borrowers can often make great accounting (but not cash) profits for many years as asset prices rise. Some even use their paper profits to buy out Hedge borrowers and then leverage up those assets as well. Eventually, the credit cycle turns and assets prices fall. Ponzi borrowers fall first, followed by Speculative borrowers, as lenders reduce their risk appetite at the same time as asset prices are falling. The combination of many distressed sellers, few buyers and limited ability to finance purchases means that asset price falls are sharp. Recovery often takes many years as Ponzi and Speculative borrowers are cleared out. So what does this practically look like?

In the years leading up to the recent financial crisis Australian companies such as Allco, Babcock and Brown, and Centro didn’t generate sufficient cashflow from their assets to make any meaningful reductions in their debt levels or to pay dividends to their shareholders. However, by revaluing their assets higher each year and borrowing against those increased values they were able to continue to operate and pay dividends to their shareholders. The rapidly growing paper profits encouraged investors to buy their shares and lenders viewed the increasing market capitalisation as a buffer against losses. Rather than looking through to see the very highly leveraged underlying assets, lenders focussed on the apparently low gearing at the parent or holding company level. When asset values fell and credit criteria tightened, each of the three became forced sellers of assets and ended up insolvent, or effectively insolvent. Consequently, lenders suffered great losses. Now we have the theoretical framework, we can apply it to residential property.

What Caused the US House Price Bubble?

Most commentaries on the US house collapse seem to start with the view that someone must be blamed so the arguments then get built around that. I’m sure you’ve read articles that blame banks, securitisation, CDOs, regulators, a lack of regulation, politicians, rating agencies or even the unsophisticated borrowers themselves. As an investor I don’t care whose fault it is, I just want to avoid the losses if another bubble arises. Therefore, my focus is on the numbers and the behaviours, which point out the warning signs for future bubbles.

The high level detail of the downturn in US house prices is generally known, with the peak (July 2006) to current fall averaging 20.3% across the twenty major cities in the Case-Schiller index. One step into the detail shows that house price falls are far from uniform. Las Vegas has fallen by 48.6%; Phoenix, Miami and Tampa are also down by more than a third; and Denver and Dallas are now setting new high marks. A further step into the detail shows even more variance, with recently developed suburbs in some cities now virtually ghost towns whilst older established suburbs might be showing no losses or healthy increases. It’s almost never as easy as simply looking at the averages.

For those who’ve never dug into the detail, the fundamentals of the home lending markets 7-10 years ago in the US were truly shocking and look almost nothing like the residential lending that occurs in Australia today. Without oversimplifying, here are three major ways that the lending markets are different:

- US residential lending markets operate primarily as an originate to on-sell system, whereas Australia has an originate and hold system. The vast majority of home loans in the US were, and still are, either on-sold to Fannie Mae or Freddie Mac, or securitised and sold through the capital markets. This distinction is important as US loan originators are often rewarded solely for volume whereas Australian lenders are profiting from the net interest margin (this is the spread after losses are taken into account between the lender’s borrowing costs and the interest rate charged to the home owner).

- Lending standards in the US in years leading up to 2006 progressively worsened with NINJA loans (no income, no job, no assets) showing that in some cases no standards existed at all. Some borrowers were literally moving from the trailer park to a McMansion on the back of 100-125% LVR loans, i.e. you could borrow more than the value of the house. Fraudulent or non-existent documentation was not a problem for many lenders with “liar loans”, another euphemism of the times. Altogether, this resulted in millions of Ponzi borrowers who had no chance of being able to make the repayments on their substantial, and often multiple, loans. To address this, loans were often structured so that repayments did not start for two years with the interest initially added to the balance owing.In Australia, the 2009 responsible lending legislation places the onus onto the lender to ensure that the borrower is able to meet repayments, “without undue hardship”. If a lender doesn’t make adequate enquiries the borrower can seek (at the lender’s expense) arbitration and potentially have the debt forgiven or reduced. When combined with the lender retaining ownership of the risk (discussed above) there are very strong economic, legal and reputational reasons to get it right.

- The third major difference is the relative ease with which US borrowers can recover from defaulting on their loans. In some US states, lenders have no recourse to the borrower in the event of a default. Even when the lender does have a legal right to pursue a borrower, the legal system often makes it impractical or uneconomic to pursue a borrower to make up a shortfall. Borrowers who have defaulted will have a black mark on their record which impacts the cost of their future borrowing, but it is by no means a road block to borrowing in the future.In Australia, recourse lending is standard. Financiers typically exercising their rights to pursue a borrower to bankruptcy when they believe other assets are available to repay a shortfall. Bankruptcy is a punitive process, with individuals being stripped of essentially all of their meaningful assets and losing half of their discretionary income for three years. Bankrupts are all but shutout of prime loans for the rest of their lives. Credit must instead be obtained through non-conforming lenders that charge higher interest rates and demand larger down payments in order to take on the risk.

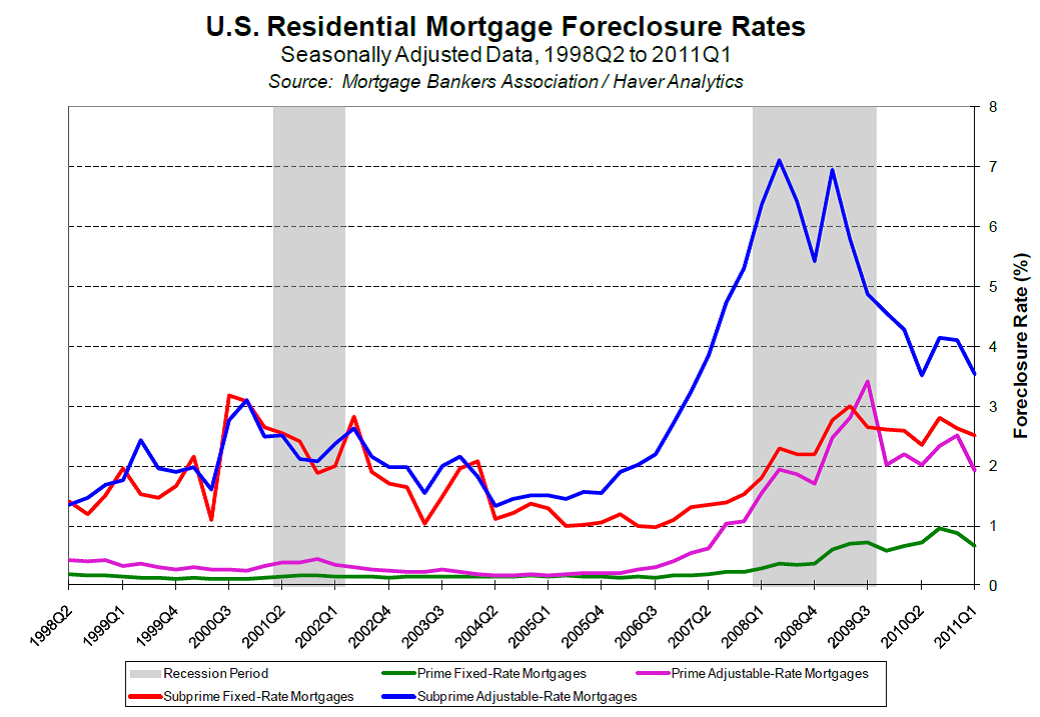

The key point from the above comparison is that Ponzi lending for residential property in the US in the mid 2000’s became common place. However, whilst that has led to massive house price falls in some areas and the collapses of some lenders and their business models, not all US lending has suffered evenly. As shown in the graph below sourced from The Federal Reserve Bank of Richmond, foreclosure (repossession) rates on variable rate subprime mortgages have been at least five times higher than fixed rate prime mortgages over the last fifteen years. (Subprime means the borrower has a reduced ability to currently service a loan and/or has had historical payment issues. Prime means the borrower exhibits both a good credit history and current financial position.)

The graph above only compares the label on the mortgage type. However it shows the potential for great variation in performance amongst different quality borrowers. When comparing hard data such as the relative level of home owner equity, the correlation between low equity and high repossession/loss rates is even stronger.

Does Australian Currently Have a House Price Bubble?

Going back to the Minsky description, Ponzi borrowers are those whose earnings from the asset are less than the interest payments. At the most basic level, with mortgage rates starting at around 5% and net rental returns of 2-4%, investors gearing a property more than 50% could be classified as Speculative. Those above 80% almost certainly meet the definition of Ponzi. This basic level analysis ignores the impact of income other than from the asset, which can include regular employment and earnings from other investments.

When Australian lenders assess the ability of a borrower to meet their obligations they typically build in buffers to ensure a borrower has some capability to withstand higher interest rates or changes in their financial situation. Firstly, whilst a borrower may be taking out a loan with a current interest rate of 5%, conservative lenders would assume a higher interest rate, such as 8% in testing their ability to service the loan. Secondly, borrowers are assumed to have minimum living expenses, so that a decent lifestyle can be maintained whilst servicing the loan. Thirdly, income is stressed with overtime and bonus income reduced or excluded from calculations. Rental income is reduced to below what would be considered market rent. No stress test can cover the impact of long term unemployment, however by ensuring that the borrower has a sufficient down-payment the lender is substantially mitigating the risk that the property is sold in a forced sale for less than the amount owing.

When these more nuanced factors are taken into account, no Australian borrower should theoretically be able to be a Speculative or Ponzi borrower, as their income from elsewhere subsidises their earnings from the asset. However, when looking at residential property as a standalone investment, there are clearly some Speculative and Ponzi characteristics. The generally held belief that capital gains will continue to accrue at above consumer price inflation or wage inflation is another warning sign. Some combination of reduced real prices (perhaps over time by inflation) or increased rents is needed to bring back a balance at the theoretical investment level. There is enough evidence to say there is a risk, but not enough to definitively conclude there is a bubble.

What Should Potential RMBS Buyers Do?

Firstly, the greatest focus must always be on the quality of the underlying loans. Potential investors should dig into the pools and search for weak loans and lending practices that are problems waiting to happen. Borrowers with good income relative to their repayments and with substantial equity rarely lose money for a lender. Losses almost always come from marginal borrowers, who have limited equity and are stretching to meet the repayments.

Secondly, it is right to be conservative and to build in a margin of safety when making any investment including Australian RMBS. That’s why I start with the base case assumption that Australian house prices will fall by 20% in nominal terms when I’m stress testing RMBS. Downside scenarios are also run with 30% and 40% reductions in house prices. Thirdly, Australian RMBS is relatively under-researched with a limited number of participants investing below AAA. Whilst the expected risk/return pay-off exceeds other classes of credit, liquidity is limited. In an economic downturn, holders should assume liquidity will be difficult to find at a decent price.

Conclusion

Having reviewed the theory and international experience, there are warnings signs pointing to the possibility of a bubble in Australian house prices. If you believe that house prices could fall by 40% or more in nominal terms, avoid Australian RMBS. You may not lose any money if such a fall occurs and you hold to maturity what you have bought, but the price volatility will almost certainly be substantial. However, if this is your view, to be consistent you’d also sell your house, any investment properties, any bank related securities, and make sure your term deposits and bank accounts are covered by the government guarantee. Whilst conservative RMBS can be stressed by large falls in house prices, the Australian banks with their high loan to valuation lending, personal loans and credit cards are arguably far more exposed to a substantial and sustained fall in house prices and consumer incomes.